THE RISKS

WITHOUT INSURANCE

There is the risk of spending down assets to qualify for Medicaid (Welfare) then Medicaid can have your estate repay Medicaid for your care costs.

The only protection from Medicaid spend-down and estate recovery is with a Partnership qualified long term care insurance policy.

There is no additional cost for a Partnership policy. The policy only has to meet your state's requirements.

Only traditional long term care insurance policies can be Partnership. Not all companies' policies are Partnership in every state because Medicaid laws differ between states.

Other options such as life insurance (hybrid) or annuities you can use for long term care are not Partnership qualified.

Some may try to transfer assets out of their name:

1. Must complete 60 months before applying for Medicaid.

2. Only an irrevocable trust is Medicaid proof (you no longer control the asset(s), and is subject to the 60 month rule.

If care only cost $6000 a month that's $216,000 in 3 years. Where would the money come from? From savings, retirement, and if that's gone Medicaid will pay and can put a lien on your house for repayment.

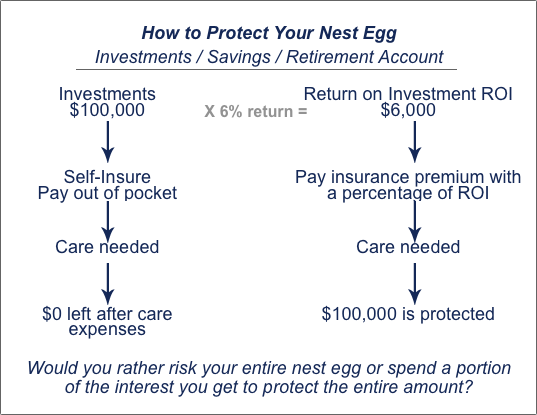

Some say they'll invest rather than insure. According to Schwab Center for Investment Research every $1000 needed for care would need $230,000 in assets earning 5.2% without dipping into principal. For a $6000 a month cost you would need $1,380,000.

TIMING

The majority of inquiries for insurance who receive quotes do not insure. They usually think "I'm OK today ... I'll be OK tomorrow."

Problem is that thought convinces us to not act now.

How much notice do we get when our health changes?

There are 10,000 reasons someone is declined for this insurance, you must buy it before you need it, even before the diagnosis!

The cost of a policy is based on: age, health and benefits.

We are here to answer any questions about Partnership.

Only you can protect your assets!

Get started, get a quote, then insure.

|